Empowering Virtual Assistants: Conversational AI Technology

Updated at Jul 29, 2026

9 min to read

Certain stocks exhibit consistent trends, while others don't. Despite drops, some companies' stock prices rebound. The common solution for both scenarios is time series models.

According to a recent study by the University of California, Berkeley, Autoregressive models are one of the most commonly used methods for time series forecasting.

The values of past and present time series frequently overlap. As a result, such data exhibit autocorrelation. As a result, knowing a product's current pricing allows us to anticipate its valuation tomorrow roughly.

So, in this article, we will explain the autoregressive model that captures this correlation.

Understanding and identifying these different time series patterns is crucial for choosing appropriate modeling techniques and accurately forecasting future values. It allows analysts to apply specific methods tailored to the patterns observed in the data, improving the accuracy of time series forecasting models.

Time series data refers to a sequence of data points collected over time, where the values are recorded at regular intervals. It represents the evolution of a variable or phenomenon over a specific period. The data points are typically indexed by the time of collection, allowing for analysis of trends, patterns, and dependencies within the data.

Time series data can be univariate, consisting of a single variable recorded over time, or multivariate, where multiple variables are observed simultaneously. Examples of time series data include stock prices, temperature readings, sales figures, and economic indicators.

Time series data often exhibit specific patterns that can be categorized into different types:

The order of autoregressive models denoted as p, represents the number of lagged values used to predict the current value. Selecting the appropriate order is crucial in autoregressive modeling.

A higher order (more significant p) allows for capturing complex dependencies but may increase model complexity and risk overfitting.

Conversely, a lower order may oversimplify the model and fail to capture essential dynamics in the data.

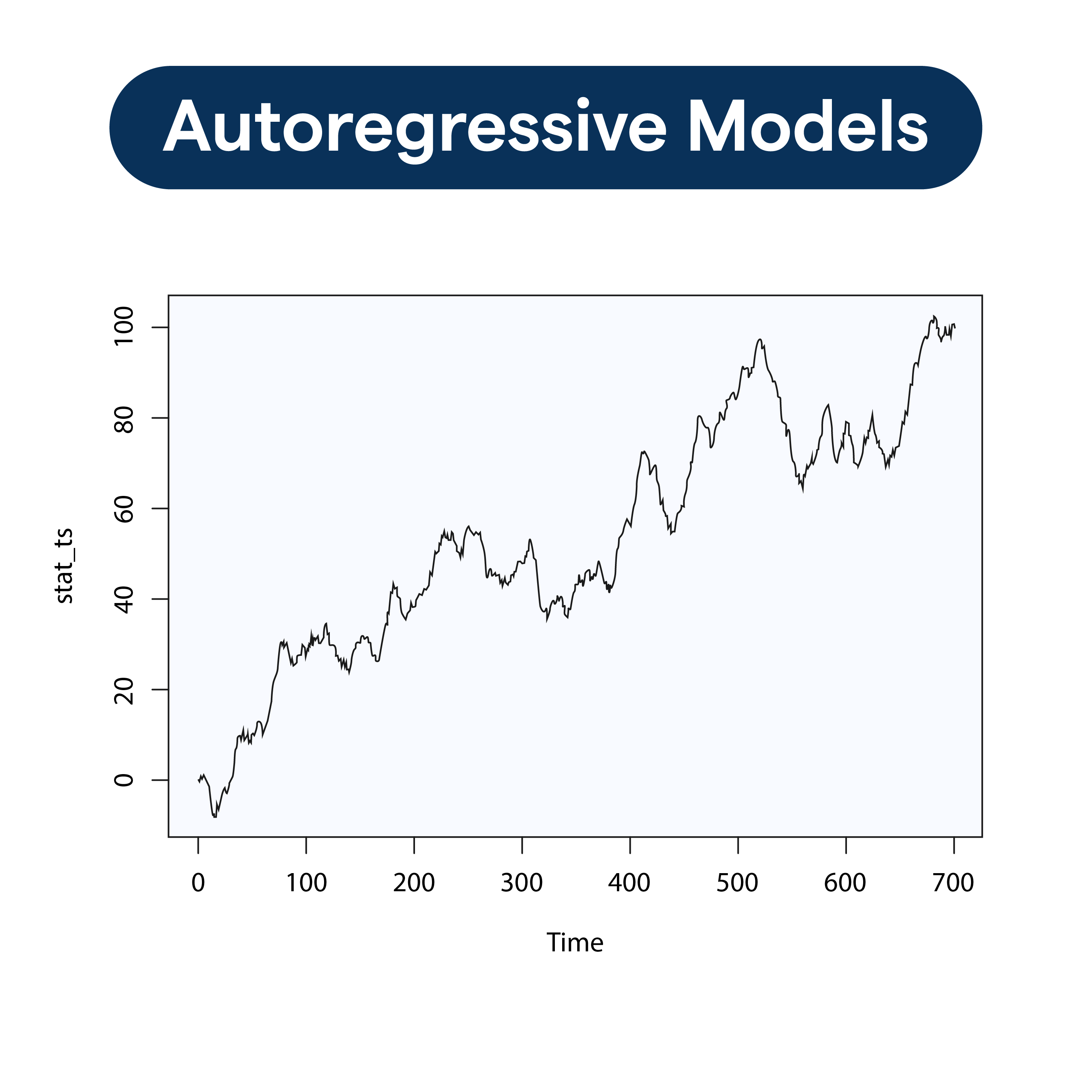

Autoregressive models are statistical models used to predict future values of a variable based on its past values.

The term "autoregressive" implies that the current value of the variable is regressed on its lagged (past) values.

The primary components of autoregressive models are the current value of the variable (dependent variable) and one or more of its lagged values (independent variables).

Autocorrelation refers to the correlation between a variable and its lagged values. It measures the degree of relationship between observations at different time points. Autocorrelation at lag k, denoted as AC(k), quantifies the linear association between a variable at time t and its value at time t-k.

Lag refers to the time gap between the current observation and its lagged value. In autoregressive models, the choice of lag is crucial as it determines the number of past values used in predicting the current value. Lag k indicates that k previous observations are considered in the model.

Stationarity is a fundamental property of time series data important for autoregressive modeling. A stationary time series exhibits constant statistical properties, such as constant mean, variance, and autocovariance structure.

Stationarity is crucial in autoregressive models because it ensures that the relationship between the current value and its lagged values remains stable.

When dealing with non-stationary data, the estimation and interpretation of autoregressive models can be challenging.

Therefore, it is often necessary to transform or manipulate non-stationary data to achieve stationarity before applying autoregressive modeling techniques.

Common techniques for achieving stationarity include differencing, logarithmic transforms, or seasonal adjustments.

Choosing the optimal order often involves statistical techniques like the Akaike Information Criterion (AIC) or Bayesian Information Criterion (BIC), which aim to balance model fit and complexity. Iterative approaches, such as autocorrelation and partial autocorrelation plots, can also help determine the order by examining the significant lags and cutoff points.

Understanding the concept of order is essential for building effective autoregressive models, as it influences model accuracy and interpretability.

Before building autoregressive models, it is essential to prepare the data and perform exploratory analysis.

Data preparation involves cleaning, transforming, and organizing the time series data in a format suitable for modeling. This may include handling missing values, smoothing noisy data, standardizing variables, and addressing non-stationarity issues.

Exploratory analysis aims to gain insights into the characteristics of the time series data.

It involves visualizing the data using lines, scatter, histograms, or box plots to identify trends, seasonality, outliers, or other patterns.

Exploratory analysis also helps in understanding the level of autocorrelation and determining the appropriate order for the autoregressive model.

The order of the autoregressive model, denoted as p, determines the number of lagged values used to predict the current value. Determining the order is crucial, as an inappropriate choice can lead to poor model performance. There are several approaches to determine the order, including:

Once the order is determined, estimating the model coefficients is next. There are various methods for estimating the coefficients in autoregressive models, including:

If you are the one who likes the no coding chatbot building process, then meet BotPenguin, the home of chatbot solutions. With all the heavy work of chatbot development already done for you, simply use its drag-and-drop feature to build an AI-powered chatbot for platforms like:

After estimating the model coefficients, assessing the model's performance and evaluating its accuracy is essential. This involves using appropriate metrics to measure how well the autoregressive model fits the data and predicts future values. Common accuracy metrics for time series models include:

Other metrics such as R-squared, Akaike Information Criterion (AIC), or Bayesian Information Criterion (BIC) can also provide insights into the model's goodness of fit and allow for model comparison.

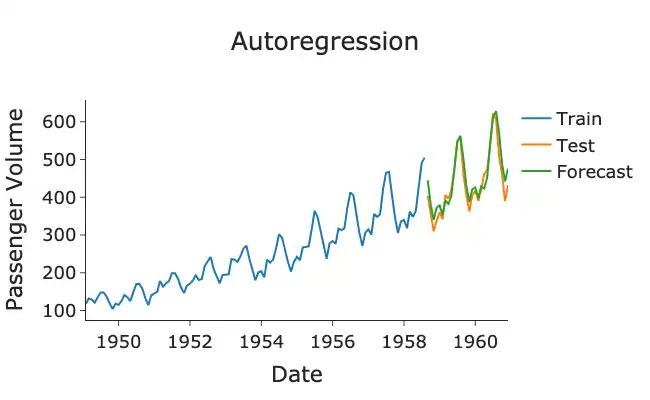

Autoregressive models can be utilized for forecasting future values of a time series variable based on its past values. Once an autoregressive model is built and its coefficients are estimated, it can generate predictions for future time points.

By using previous values of the variable, the model can capture the inherent patterns and dependencies in the data, allowing for reasonably accurate predictions.

The autoregressive model can be recursively applied to make future predictions by using the predicted values as inputs for the subsequent time points. For example, if an AR(p) model is built, the model equation can forecast the value at time t+1 by substituting the lagged values up to t with the corresponding predicted values.

After generating forecasts with the autoregressive model, assessing the predictions' accuracy and understanding the model's limitations is crucial. Several techniques can be employed to evaluate the forecast accuracy:

While autoregressive models provide a solid foundation for time series forecasting, some advanced techniques and considerations can enhance their performance:

The autoregressive model forecasts the future based on past data. Technical analysts widely use them to forecast future security prices. Time series values are associated with their predecessors and successors in this analysis.

Autoregressive models use the squared coefficient of previous values to predict the next value in a vector time series.

Autoregressive models are statistical models that have proven effective for us in various applications, including time series and financial forecasting. They are also used to build models from time series data.

An autoregressive model is used for time series forecasting. It relies on the relationship between past values of the variable and its current value to make predictions for the future.

The order of an autoregressive model determines the number of lagged values used for prediction. It can be determined using autocorrelation, partial autocorrelation functions, or information criteria.

Some common techniques for estimating autoregressive model coefficients include ordinary least squares, Yule-Walker equations, and maximum likelihood estimation. These methods determine the relationship between current and past values of the time series.

The accuracy of autoregressive model forecasts can be evaluated using metrics such as mean absolute error, root mean squared error, and mean absolute percentage error. Backtesting and analyzing residuals can also provide insights into model performance.

Autoregressive models typically assume the absence of seasonality. However, extensions like SARIMA or Fourier terms can be included to capture seasonal patterns and improve forecast accuracy.

Yes, there are advanced techniques to enhance autoregressive model forecasting. These include incorporating exogenous variables that may influence the time series, model selection and combination approaches, and online learning techniques for real-time forecasting.

Subscribe to Our Newsletter

Get the latest business insights straight into your inbox.

Checkout our related blogs you will love.

Updated at Jul 29, 2026

9 min to read

Updated at Jul 29, 2026

11 min to read

Updated at Jul 28, 2026

10 min to read

Updated at Jul 13, 2026

7 min to read

Updated at Jul 3, 2026

10 min to read

Updated at Jul 2, 2026

8 min to read

Table of Contents