W

Wayne Quek

CFA, Home Loan Whiz, Singapore

★★★★★

BotPenguin changed how we handle client inquiries. Every WhatsApp message now gets an instant, professional response; it feels like having an assistant who never sleeps.

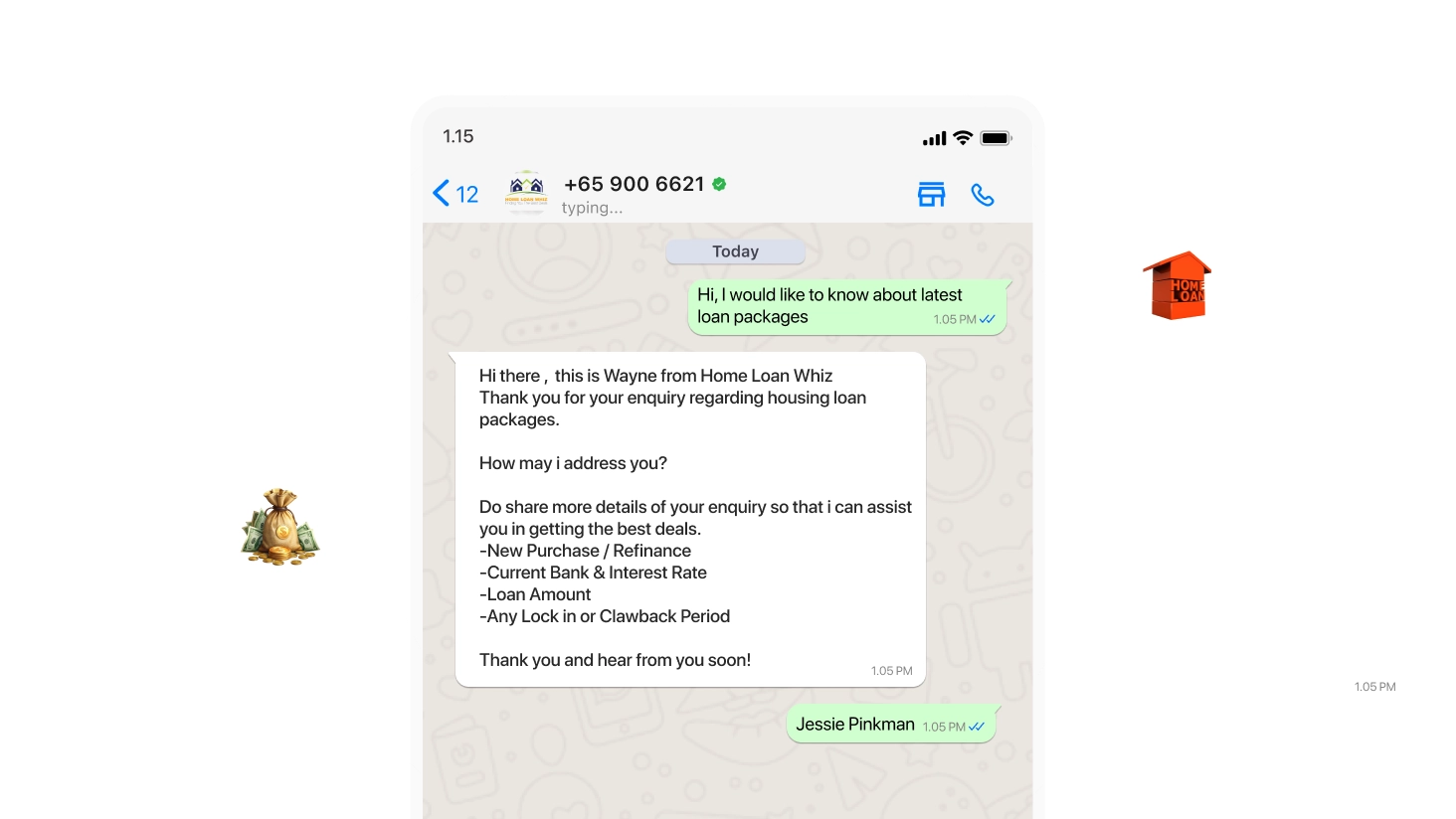

Home Loan Whiz - Case Study

Home Loan Whiz used a mortgage chatbot setup to pre-qualify WhatsApp mortgage leads 40% faster, cover after-hours enquiries, and send advisors complete financial profiles before the first consultation.

Figures are reported by Home Loan Whiz and reflect operational data measured before and after deployment. Estimated figures are noted as such in the results table.

Mortgage Advisory / Financial Services

Singapore

B2C financial services

Lead qualification, client education, advisor routing

WhatsApp qualification automation

The Challenge

Singapore’s mortgage market is complex. Homebuyers need clarity on HDB loans, bank loans, TDSR, MSR, CPF usage, refinancing, and property eligibility before speaking meaningfully with an advisor. For Home Loan Whiz, this made lead intake time-heavy, with advisors collecting the same financial details before every serious consultation.

Buyers asked about HDB versus bank loans, CPF usage, TDSR, MSR, and refinancing triggers, consuming advisor time on basics.

Leads reached advisors without complete details like income, loan quantum, property type, employment status, or residency.

Singapore homebuyers often research mortgages at night or on weekends, and without automation these enquiries waited until the next business day.

Advisors spent early consultation time collecting data instead of giving loan guidance, limiting how many productive consultations they could handle.

Why BotPenguin

Home Loan Whiz needed a financial advisory chatbot setup that could handle Singapore mortgage intake without crossing into regulated advice. BotPenguin matched how mortgage advisory actually works in Singapore.

The workflow captured income, loan amount, property type, employment, and residency instead of using a generic lead form.

The bot collected information and educated clients, while formal financial advice stayed with licensed advisors.

Home Loan Whiz met prospects on a channel they already used and responded immediately, including after hours.

Leads could be routed by HDB, private property, commercial, or refinancing needs before advisor follow-up.

Advisors received structured profiles upfront, helping the team handle more consultations without the same manual intake work.

Implementation Journey

Days 1–3

Configured the intake flow around Singapore mortgage advisory needs, covering income, loan quantum, property type, employment, and residency.

Week 1–2

Added HDB, bank loan, TDSR, MSR, CPF, and refinancing responses, and tested routing for HDB buyers, private property clients, commercial borrowers, and refinancers.

Week 3–4

WhatsApp became the primary lead intake channel, so enquiries could be captured, educated, qualified, and routed before advisor follow-up.

Ongoing

Advisors received pre-filled profiles before calls, freeing them to spend more time on loan structuring, lender comparison, and client guidance.

Days 1–3

Configured the intake flow around Singapore mortgage advisory needs, covering income, loan quantum, property type, employment, and residency.

Week 1–2

Added HDB, bank loan, TDSR, MSR, CPF, and refinancing responses, and tested routing for HDB buyers, private property clients, commercial borrowers, and refinancers.

Week 3–4

WhatsApp became the primary lead intake channel, so enquiries could be captured, educated, qualified, and routed before advisor follow-up.

Ongoing

Advisors received pre-filled profiles before calls, freeing them to spend more time on loan structuring, lender comparison, and client guidance.

The Solution

BotPenguin deployed a home loan WhatsApp automation system that turned inbound mortgage enquiries into structured, pre-qualified leads before advisor involvement.

The bot collected gross monthly income, desired loan quantum, property type, employment category, and residency status, replacing unstructured intake.

Common questions and guidance on loan considerations, eligibility factors, and refinancing topics meant clients reached advisors with a clearer understanding.

Qualified leads were routed to the right specialist based on property type and enquiry need across HDB, private property, commercial, and refinancing.

Enquiries were captured and qualified outside business hours, giving 100% after-hours coverage instead of waiting for manual callbacks.

The bot collected information and provided general education, while formal financial advice remained with licensed advisors.

Want to pre-qualify mortgage leads before advisor calls?

Capabilities Used

| Feature | How it was used |

|---|---|

| WhatsApp Business Automation | Used as the core intake channel for mortgage enquiries. |

| Lead Qualification Flows | Captured income, loan quantum, property type, employment, and residency. |

| FAQ Automation | Explained HDB loans, bank loans, TDSR, MSR, CPF usage, and refinancing. |

| Lead Routing | Routed qualified leads to HDB, private property, commercial, or refinancing specialists. |

| 24/7 Availability | Captured and qualified after-hours mortgage enquiries. |

| Structured Data Collection | Created pre-filled financial profiles before advisor consultations. |

| Human Handoff | Sent qualified leads to advisors for formal financial guidance. |

Results

| Metric | Before | After |

|---|---|---|

| Lead qualification speed | Advisors qualified leads manually | 40% faster qualification through WhatsApp intake |

| After-hours coverage | Evening and weekend enquiries waited | 100% after-hours lead coverage |

| Consultant workload | Advisors handled repetitive data collection | 60% reduction in consultant workload |

| Advisor capacity | Capacity depended on manual qualification | Estimated 25 to 30% more consultations per day |

| Routing accuracy | Specialist assignment required manual review | Estimated 90 to 95% correct specialist routing |

| First consultation efficiency | Advisors spent time gathering basic details | Estimated 20 minutes saved per call |

| Qualification standard | Lead quality varied by enquiry | Every lead arrived with structured financial details |

Strategic Business Impact

BotPenguin helped Home Loan Whiz separate data collection from advisory work. Mortgage leads could now be qualified on WhatsApp before an advisor joined the conversation, which matters because mortgage advisory depends on both speed and precision.

This matters as mortgage advisory depends on both speed and precision.

This BotPenguin home loan chatbot case study shows how a mortgage advisory firm can use a loan inquiry chatbot to improve qualification speed without replacing licensed advisor judgment.

CFA, Home Loan Whiz, Singapore

BotPenguin changed how we handle client inquiries. Every WhatsApp message now gets an instant, professional response; it feels like having an assistant who never sleeps.

Use BotPenguin to pre-qualify home loan enquiries, educate clients, route leads to the right advisor, and cover after-hours WhatsApp enquiries.

Automate Your Mortgage Lead Qualification on WhatsApp Mid intent100%inquiries answered instantly

55% lower workload and 45% faster qualification of international payment requests.

50%reduction in workload

3x faster responses and 100% automated data sync into CRM and Tally.

800+qualified leads

100% lead auto-transfer into Bitrix CRM with under 60-second delivery.

Use BotPenguin to pre-qualify home loan enquiries, educate clients, route leads to the right advisor, and cover after-hours WhatsApp enquiries.

How does a WhatsApp chatbot automate home loan inquiries in Singapore?

A WhatsApp chatbot automates home loan inquiries by collecting income, loan amount, property type, employment category, and residency status. Home Loan Whiz used BotPenguin to pre-qualify WhatsApp mortgage leads 40% faster.

Can a mortgage chatbot qualify leads based on income and property type?

Yes. A mortgage chatbot can qualify leads by collecting gross monthly income, desired loan quantum, property type, employment status, and residency details before advisor follow-up.

Is BotPenguin’s WhatsApp chatbot compliant with MAS regulations in Singapore?

BotPenguin can support a compliance-safe workflow when configured correctly. For Home Loan Whiz, the bot collected information and provided general education, while formal financial advice remained with licensed advisors.

How did Home Loan Whiz automate WhatsApp inquiries?

Home Loan Whiz used BotPenguin to capture, qualify, educate, and route inbound mortgage leads before advisor involvement, which also helped cover after-hours enquiries automatically.

What types of mortgage questions can a chatbot handle automatically?

A mortgage chatbot can answer first-level questions about HDB loans, bank loans, TDSR, MSR, CPF usage, property type, refinancing triggers, and basic eligibility factors.

How long does it take to deploy a home loan chatbot in Singapore?

Deployment depends on the qualification flow, advisor routing rules, and compliance requirements. Home Loan Whiz followed a staged setup covering WhatsApp configuration, Singapore mortgage content, routing tests, and live deployment.